Over the past year or so, some new, alternative mortgage programs have been developed in order to meet the needs of borrowers with unique circumstances/needs. Generally, these programs require 20% down and require credit scores of 620 or above.

Bank Statement Program: This program has been developed to assist self-employed borrowers in qualifying for a mortgage by utilizing an average of business deposits for income qualifying rather than using information on their personal and business federal income tax returns. Typically, a 12 or 24 month average is used to make the income determination for qualifying. A 50% expense ratio is used; therefore, that average is then divided by 2 in order to determine qualifying income. The Lender determines which deposits are considered to be “business deposits” when making this calculation.

1099-only Program: This program has also been developed to assist self-employed borrowers in qualifying for a mortgage by using 75% of 1099-MISC income received and then averaged over a 2 yr. period.

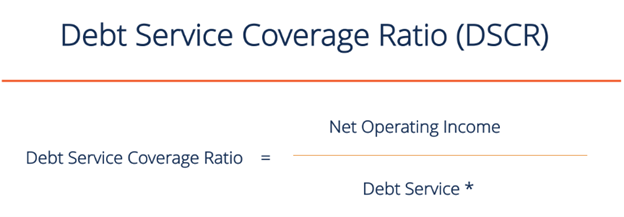

DSCR Program: DSCR stands for Debt Service Coverage Ratio. This program is used for residential investment property transactions and the Debt Service Coverage Ratio* must generally be at or over 1.00. Only income used for qualifying is that generated from the rent produced from the investment property. This can be used for up to a 4 unit property where all units are residential use. Minimum loan amount is $150000. Borrower must have at least 12 mos of landlord/property management experience in the past 3 yrs.

No Ratio Program: This program is used for residential investment property transactions only. It requires no debt ratio calculation be made of any kind.

*Debt Service equals the PITI payment for the new mortgage.